![]()

[2026年01月最新リリース]GFMC問題集でGovernment Financial Manager認証

最新の完璧なGFMC問題集問題と解答で100%パスさせます

AGA GFMC 認定試験の出題範囲:

| トピック | 出題範囲 |

|---|---|

| トピック 1 |

|

| トピック 2 |

|

| トピック 3 |

|

| トピック 4 |

|

| トピック 5 |

|

質問 # 41

Using Benford Digital Analysis, an auditor can identify potential fraud when

- A. an employee receives kickbacks from real estate developers.

- B. a higher-than-expected number of payment amounts to one vendor start with the number three.

- C. a large number of contracts are awarded to one vendor.

- D. a large contract is awarded to the director's close relative.

正解:B

解説:

* Benford's Law and Fraud Detection:

* Benford's Lawis a statistical principle that predicts the frequency of leading digits in naturally occurring datasets.

* Deviations from the expected distribution (e.g., a higher-than-expected frequency of a specific leading digit) can indicate manipulation or fraud.

* For example, if too many payments start with the number "3," it suggests potential tampering.

* Explanation of Answer Choices:

* A. A higher-than-expected number of payment amounts to one vendor start with the number three: Correct. This aligns with how Benford's Law is used to detect anomalies in numerical data.

* B. A large number of contracts are awarded to one vendor: While concerning, this is not related to Benford's Law.

* C. A large contract is awarded to the director's close relative: This indicates a conflict of interest but is unrelated to Benford's Law.

* D. An employee receives kickbacks from real estate developers: This is fraud but cannot be identified using Benford's Law.

:

Association of Certified Fraud Examiners (ACFE),Fraud Detection Using Benford's Law.

GAO,Fraud Risk Management Framework.

質問 # 42

To support optimal cash management vendor payment procedures, invoices with discount terms should be paid

- A. on the due date, unless a charge is assessed for late payment.

- B. after the due date to increase cash flow.

- C. on the discount date.

- D. prior to the due date to improve credit rating.

正解:C

解説:

Why Pay on the Discount Date?

* Discount termsare offered by vendors to encourage early payment, such as "2/10, net 30" (2% discount if paid within 10 days). Paying on the discount date ensures the organization takes advantage of cost savings while still making timely payments.

* This approach optimizes cash management by reducing payment obligations while maintaining good vendor relationships.

Why Other Options Are Incorrect:

* A. After the due date:Late payments can damage vendor relationships and incur penalties.

* B. Prior to the due date:Paying too early does not provide additional benefits and can unnecessarily deplete cash reserves.

* C. On the due date:If a discount is offered, waiting until the due date means missing the opportunity to save money.

References and Documents:

* GAO Financial Management Guide:Recommends paying invoices with discounts on the discount date to maximize cost savings.

* Best Practices in Governmental Cash Management (AGA):Highlights the importance of managing vendor payments to take advantage of discounts.

質問 # 43

An analyst has identified several variables that may be impacting state lottery ticket sales, including investments in advertising, potential pay-out amounts and the size of lottery cards. Which of the following techniques would help determine the extent to which each variable is impacting sales?

- A. narrative analysis

- B. content analysis

- C. regression analysis

- D. cost-benefit analysis

正解:C

解説:

* Regression Analysis:

* Regression analysis is a statistical technique used to examine the relationships between a dependent variable (e.g., lottery ticket sales) and one or more independent variables (e.g., advertising, potential payouts, size of lottery cards).

* This method helps quantify the extent to which each variable impacts sales.

* Explanation of Answer Choices:

* A. Content analysis: Incorrect. This method is used to analyze qualitative data (e.g., text or media) rather than numerical relationships.

* B. Cost-benefit analysis: Incorrect. This technique evaluates the costs and benefits of a decision but does not identify the relationships between variables.

* C. Regression analysis: Correct. This technique determines the impact of multiple variables on a single outcome.

* D. Narrative analysis: Incorrect. This is used to analyze stories or qualitative information, not numerical data.

:

Association of Government Accountants (AGA),Data Analytics and Predictive Techniques in Government.

U).S. Census Bureau,Statistical Techniques for Economic Analysis.

質問 # 44

The ratios used to determine an organization's ability to meet its creditor's demands are

- A. liquidity ratios.

- B. turnover ratios.

- C. budgetary cushion ratios.

- D. debt burden ratios.

正解:A

解説:

What Are Liquidity Ratios?

Liquidity ratios are financial metrics used to measure an organization's ability to meet its short-term financial obligations as they come due. These ratios assess whether the organization has sufficient liquid assets (like cash, receivables, or short-term investments) to cover its current liabilities (debts or obligations due within a year).

Why Are They Relevant to Creditors?

Creditors care deeply about an entity's ability to repay its debts in a timely manner. Liquidity ratios provide a snapshot of the organization's financial health and give insight into its capacity to meet short-term demands.

They are essential tools in evaluating whether a government entity (federal, state, or local) or any other organization can pay its creditors without needing to secure additional financing or liquidate long-term assets.

Common Liquidity Ratios:

The most commonly used liquidity ratios are:

* Current Ratio:This measures the organization's ability to pay off its current liabilities with current assets.Formula:Current Assets ÷ Current Liabilities

* Quick Ratio (Acid-Test Ratio):A stricter version of the current ratio, it excludes less liquid assets (like inventory) to assess the organization's immediate ability to pay short-term debts.Formula:(Current Assets - Inventory) ÷ Current Liabilities

* Cash Ratio:Focuses only on the most liquid assets, such as cash and cash equivalents.Formula:Cash + Cash Equivalents ÷ Current Liabilities How Do Liquidity Ratios Apply to Governmental Accounting?

In governmental accounting, liquidity ratios are crucial for determining whether a governmental entity has the financial flexibility to manage short-term obligations like accounts payable, payroll, and other operating costs.

For example:

* State and local governments use liquidity ratios to show stakeholders their ability to sustain operations without financial strain.

* Government-wide financial statements (under GASB standards) often emphasize liquidity to demonstrate fiscal health to bondholders and credit rating agencies.

Why Not Other Ratios?

* A. Budgetary Cushion Ratios:These focus on the organization's ability to withstand revenue shortfalls and maintain budgetary reserves, not specifically on meeting creditor demands.

* C. Debt Burden Ratios:These measure the overall burden of debt on the organization but don't directly address short-term liquidity or solvency.

* D. Turnover Ratios:These evaluate operational efficiency (e.g., how quickly assets like inventory are converted into revenue), which doesn't directly relate to creditor demands.

References and Documents:

* Government Financial Manager (GFM) Competency Framework by the Association of Government Accountants (AGA):Section on "Financial Analysis" emphasizes the importance of liquidity ratios in assessing short-term solvency for government entities.

* GASB Concepts Statement No. 1:Discusses the need for governmental financial reporting to provide information on financial condition, including short-term liquidity.

* AGA Performance Management Framework Guide (2023):Highlights liquidity ratios as critical tools for demonstrating fiscal responsibility and transparency in public sector financial management.

質問 # 45

In state and local financial audits, material weaknesses must be reported to the

- A. governing body.

- B. legislature.

- C. taxpayers.

- D. local media.

正解:A

解説:

What Are Material Weaknesses?

* Amaterial weaknessin internal control is a deficiency or combination of deficiencies that creates a reasonable possibility of a material misstatement in the financial statements that would not be prevented or detected in a timely manner.

* In the context of state and local financial audits, material weaknesses must be reported to those charged with governance, as they are responsible for oversight and corrective actions.

Why Is the Governing Body the Correct Answer?

* Thegoverning body(e.g., city council, county board, or state commission) is directly responsible for overseeing the entity's financial operations and ensuring accountability. Reporting material weaknesses to them ensures that corrective actions can be implemented to strengthen internal controls.

* Auditors communicate such findings through anaudit reportor amanagement letteraddressed to the governing body.

Why Other Options Are Incorrect:

* A. Legislature:The legislature may have oversight of state budgets and appropriations but is not the direct governing body for financial audits.

* C. Taxpayers:While transparency is important, material weaknesses are not directly reported to taxpayers. They may be disclosed in public audit reports, but taxpayers are not the primary audience.

* D. Local media:Material weaknesses are not formally reported to the media; their disclosure depends on the entity's public reporting processes.

References and Documents:

* GAO Yellow Book (GAGAS):Requires auditors to report material weaknesses to those charged with governance.

* GASB (Governmental Accounting Standards Board):Emphasizes the importance of communicating significant audit findings to governing bodies.

* AICPA Audit Standards (AU-C 265):Requires auditors to communicate material weaknesses to management and those charged with governance.

質問 # 46

One of the minimum components of a government financial system is

- A. automated transaction processing.

- B. debt-reduction analysis.

- C. performance management reporting.

- D. general ledger account definition.

正解:D

解説:

* Minimum Components of a Government Financial System:

* A general ledger is the foundation of any financial system, providing a complete record of all financial transactions.

* The definition ofgeneral ledger accountsensures proper classification, tracking, and reporting of financial activities.

* Explanation of Answer Choices:

* A. Automated transaction processing: Incorrect. While automation is beneficial, it is not a

"minimum" requirement. Manual systems can still exist.

* B. Debt-reduction analysis: Incorrect. This is a financial management activity, not a core component of the financial system.

* C. Performance management reporting: Incorrect. Performance reporting is separate from the foundational financial system.

* D. General ledger account definition: Correct. This is a fundamental element of any government financial system.

:

GAO,Standards for Internal Control in the Federal Government (Green Book).

GASB,Codification of Governmental Accounting and Financial Reporting Standards.

質問 # 47

One of the five components of COSO ERM is

- A. complex calculations.

- B. performance.

- C. accepting risk.

- D. changing environment.

正解:B

解説:

What Is COSO ERM?

TheCOSO Enterprise Risk Management (ERM) Frameworkis a widely accepted framework that helps organizations identify, assess, and manage risks while creating value. The five components of COSO ERM are:

* Governance and Culture

* Strategy and Objective-Setting

* Performance

* Review and Revision

* Information, Communication, and Reporting

Why Is Performance a Key Component?

* ThePerformancecomponent focuses on identifying, assessing, and prioritizing risks to achieving an organization's objectives. It includes implementing risk responses (e.g., avoiding, reducing, sharing, or accepting risks) and monitoring their effectiveness.

Why Other Options Are Incorrect:

* B. Changing Environment:This is not a COSO ERM component but a general factor influencing risk management.

* C. Complex Calculations:This is not relevant to COSO ERM.

* D. Accepting Risk:While accepting risk is part of risk responses, it is not one of the five COSO ERM components.

References and Documents:

* COSO ERM Framework (2017):Details the five components of ERM and their application in managing risks.

質問 # 48

Use of a lockbox eliminates

- A. internal office processing delays occurring prior to making deposits.

- B. delays in the availability of funds after transaction initiation.

- C. the writing of checks against insufficient funds.

- D. mail and check-clearing time.

正解:A

解説:

What Is a Lockbox?

* Alockboxis a service provided by banks to streamline the collection of payments. Customers send payments directly to a bank-managed P.O. box, where the bank processes and deposits them on behalf of the organization.

Why Does a Lockbox Eliminate Internal Office Processing Delays?

* Payments are sent directly to the bank, bypassing the organization's internal mail and deposit processes.

This eliminates delays caused by handling checks internally and ensures quicker access to funds.

Why Other Options Are Incorrect:

* B. Mail and check-clearing time:Lockboxes reduce internal processing delays but do not affect the mail delivery time or bank check-clearing processes.

* C. Delays in the availability of funds after transaction initiation:Fund availability depends on banking processes, not the lockbox.

* D. Writing of checks against insufficient funds:Lockboxes do not prevent the issuance of bad checks.

References and Documents:

* Treasury Financial Manual:Describes lockboxes as tools to reduce internal delays in payment processing.

* GAO Financial Management Best Practices:Highlights the benefits of lockboxes in expediting deposits.

質問 # 49

In defining the audit objectives of a performance audit, auditors should evaluate whether the audited entity has

- A. internal controls in place.

- B. updated its financial reports' MD&A.

- C. updated its vision and strategic mission statements.

- D. corrective actions to address prior findings and recommendations.

正解:D

解説:

* Performance Audit Objectives:

* Performance audits evaluate whether government entities are operating efficiently, effectively, and in compliance with applicable laws.

* A critical aspect is assessing whether the entity has implementedcorrective actionsin response to prior audit findings and recommendations, as this demonstrates accountability and progress.

* Explanation of Answer Choices:

* A. Updated its vision and strategic mission statements: Incorrect. While strategic planning is important, it is not the primary focus of performance audit objectives.

* B. Corrective actions to address prior findings and recommendations: Correct. Addressing prior findings is a key objective to ensure identified issues have been resolved.

* C. Updated its financial reports' MD&A: Incorrect. MD&A (Management's Discussion and Analysis) is related to financial reporting, not performance audits.

* D. Internal controls in place: Incorrect. While internal controls are reviewed, the focus here is on corrective actions to past findings.

:

GAO,Government Auditing Standards (Yellow Book).

GAO,Performance Auditing Guidance.

質問 # 50

The Federal Credit Reform Act requires complex calculations, which are likely to include errors. This is an example of

- A. control risk.

- B. detection risk.

- C. audit risk.

- D. inherent risk.

正解:D

解説:

Definition of Inherent Risk:

Inherent risk refers to the risk of material misstatement in financial statements or other reports due to the nature of the subject matter, without considering any controls in place. It arises from the complexity, judgment, or uncertainty involved in the underlying transactions or calculations.

Why This Is Inherent Risk:

* TheFederal Credit Reform Actrequires complex calculations to estimate loan subsidies, interest rates, and cash flows. These calculations inherently involve significant judgment and estimation, making them prone to errors. This is a classic example of inherent risk because the complexity exists regardless of controls.

Why Other Options Are Incorrect:

* A. Audit Risk:This refers to the overall risk that the auditor may issue an incorrect opinion. In this case, the issue is about the inherent complexity of the calculations, not the auditor's procedures.

* B. Control Risk:This is the risk that errors will not be prevented or detected due to weak internal controls. While control risk could contribute to misstatements, it is not the primary issue in this example.

* C. Detection Risk:This is the risk that auditors will not detect a misstatement. This risk relates to audit procedures, not the inherent complexity of the calculations.

References and Documents:

* GAO Yellow Book on Risk Assessment:Explains inherent risk in the context of government financial reporting.

* AICPA Standards on Audit Risk (AU-C 315):Highlights inherent risk as arising from the nature of transactions or subject matter.

質問 # 51

All of the following ae among the stated purposes of GPRA EXCEPT to

- A. improve internal management practices.

- B. provide instructions on program reporting.

- C. help managers improve service delivery.

- D. improve program effectiveness.

正解:B

解説:

What Is GPRA?

TheGovernment Performance and Results Act (GPRA)of 1993 was designed to improve the performance of federal programs by requiring federal agencies to establish goals, measure performance, and report on their progress.

Stated Purposes of GPRA:

* Improve Service Delivery (Option A):GPRA helps agencies align performance goals with customer needs, improving service delivery.

* Improve Internal Management Practices (Option B):By requiring performance metrics and evaluations, GPRA enhances internal management and decision-making processes.

* Improve Program Effectiveness (Option D):GPRA aims to make federal programs more effective by fostering accountability and linking resources to results.

Why Option C Is Incorrect:

* GPRA does not provide detailedinstructions on program reporting.While it requires agencies to report on their performance, it does not dictate the specific steps or instructions for reporting. Instead, agencies design their own reporting processes within the GPRA framework.

References and Documents:

* Government Performance and Results Act of 1993:Stipulates the law's objectives but does not mention program reporting instructions.

* GAO Report on GPRA Implementation:Highlights GPRA's purpose to improve performance management and accountability without prescribing reporting instructions.

質問 # 52

A federal government agency that expends beyond its appropriation is in violation of the

- A. Sarbanes-Oxley Act.

- B. Antideficiency Act.

- C. Federal Managers' Financial Integrity Act.

- D. Federal Financial Management Improvement Act.

正解:B

解説:

* Antideficiency Act Overview:

* TheAntideficiency Act (31 U.S.C. §§ 1341, 1342, 1517)prohibits federal agencies from:

* Obligating or expending funds in excess of their appropriations.

* Entering into contracts without sufficient appropriated funds.

* Violating the Act is a serious matter, and agencies are required to report such violations to Congress and the President.

* Explanation of Answer Choices:

* A. Federal Managers' Financial Integrity Act: Incorrect. This Act requires agencies to assess internal controls, not monitor appropriations.

* B. Federal Financial Management Improvement Act: Incorrect. This Act focuses on improving financial systems, not budgetary compliance.

* C. Antideficiency Act: Correct. This Act directly prohibits expenditures beyond appropriations.

* D. Sarbanes-Oxley Act: Incorrect. This Act applies to corporate financial reporting, not federal appropriations.

:

Antideficiency Act (31 U.S.C. §§ 1341, 1342, 1517).

GAO,Principles of Federal Appropriations Law.

質問 # 53

When considering materiality during the planning phase for the field work for a financial audit, the dollar threshold for materiality is determined by the

- A. auditor.

- B. auditor in consultation with the auditee.

- C. audit committee.

- D. auditee.

正解:A

解説:

Materiality in Auditing:

* Materiality refers to the significance of misstatements or omissions in financial statements that could influence the decisions of users relying on those statements.

* During theplanning phaseof a financial audit, the auditor determines the dollar threshold for materiality based on professional judgment, considering the size and nature of the auditee's operations and the needs of financial statement users.

Why the Auditor Determines Materiality:

* Theauditorhas the responsibility to form an independent opinion on the financial statements and must determine materiality thresholds to design audit procedures effectively.

* Materiality thresholds guide the extent of testing and ensure the audit focuses on areas most likely to impact decision-making.

Why Other Options Are Incorrect:

* B. Auditee:The auditee provides the information, but it does not decide the materiality threshold.

* C. Auditor in consultation with the auditee:The auditor may consult with the auditee for context, but the final determination is solely the auditor's responsibility.

* D. Audit committee:While the audit committee oversees the audit, it does not set materiality thresholds.

References and Documents:

* GAAS (Generally Accepted Auditing Standards):States that materiality is determined by the auditor' s judgment.

* AICPA AU-C Section 320:Provides guidance on materiality in planning and performing audits.

質問 # 54

According to OMB Circular A-11, what analytical method should be used to measure the cost, schedule and performance goals of a capital asset acquisition project?

- A. earned value management

- B. future value

- C. regression analysis

- D. net present value

正解:A

解説:

* OMB Circular A-11 and Capital Asset Acquisition:

* OMB Circular A-11 mandates the use ofearned value management (EVM)for measuring cost, schedule, and performance goals in capital asset acquisition projects.

* EVM integrates project scope, schedule, and cost data to assess project performance and forecast outcomes.

* Explanation of Answer Choices:

* A. Earned value management: Correct. EVM is the prescribed method for tracking progress on capital projects under OMB Circular A-11.

* B. Net present value: Used for financial analysis, such as determining the economic value of future cash flows, but not for tracking project progress.

* C. Future value: Measures the value of an investment at a future point, not applicable to project tracking.

* D. Regression analysis: A statistical method for identifying relationships between variables, not for measuring project performance.

:

OMB Circular A-11,Capital Programming Guide.

U).S. General Services Administration (GSA),Earned Value Management Implementation.

質問 # 55

The legislation that expanded the requirements of audits to virtually all federal agencies is the

- A. Federal Financial Management Improvement Act of 1996.

- B. Government Management Reform Act of 1994.

- C. Accountability for Tax Dollars Act of 2002.

- D. CFO Act of 1990.

正解:C

解説:

What Did the Accountability for Tax Dollars Act Do?

* This act expanded the audit requirements tovirtually all federal agencies, not just those covered under the CFO Act of 1990.

* It mandated that agencies prepare audited financial statements to improve transparency, accountability, and the management of federal funds.

Why Other Options Are Incorrect:

* A. CFO Act of 1990:This act required audited financial statements but only applied to the 24 largest federal agencies (those covered under the Chief Financial Officers Act).

* C. Federal Financial Management Improvement Act of 1996:Focused on financial system compliance with federal accounting standards, not expanding audit requirements.

* D. Government Management Reform Act of 1994:Extended the CFO Act requirements to consolidated government-wide financial statements, not all federal agencies.

References and Documents:

* Accountability for Tax Dollars Act of 2002:Specifies the expanded audit requirements for federal agencies.

* GAO Guide on Federal Financial Management Laws:Provides a comprehensive overview of key legislation.

質問 # 56

The National Performance Management Advisory Commission established a comprehensive framework that incorporates performance measurement into the

- A. audit procedures.

- B. financial statements.

- C. internal control plan.

- D. budget process.

正解:D

解説:

National Performance Management Advisory Commission Framework:

* TheNational Performance Management Advisory Commissiondeveloped a comprehensive framework to integrateperformance measurementinto government operations.

* One of its primary goals was to incorporate performance metrics into thebudget processto align resource allocation with program outcomes.

* This ensures that budgeting decisions are informed by program performance, improving efficiency and accountability.

Why the Budget Process?

* By linking performance to budgeting, governments can prioritize funding for programs that demonstrate effectiveness and reduce funding for underperforming initiatives.

Why Other Options Are Incorrect:

* A. Internal control plan:Internal controls focus on risk management, not incorporating performance measurement.

* B. Financial statements:Performance metrics are not reported in financial statements, which focus on financial position and results.

* C. Audit procedures:Audits verify financial accuracy and compliance but do not incorporate performance measurement.

References and Documents:

* National Performance Management Advisory Commission Report (2010):Recommends integrating performance measurement into the budget process.

* GAO Guide on Performance Budgeting:Explains how performance metrics inform budget decisions.

質問 # 57

Pay.gov is an example of

- A. a concentration system.

- B. an electronic lockbox.

- C. a data warehouse system.

- D. a zero-balance account.

正解:B

解説:

What Is Pay.gov?

* Pay.govis anelectronic lockbox systemmanaged by the U.S. Department of the Treasury. It allows federal agencies to collect payments electronically, improving efficiency and reducing the time and cost associated with manual payment processing.

* It supports online payments for taxes, fees, and other government-related obligations.

Why Is It an Electronic Lockbox?

* Pay.gov consolidates and processes payments on behalf of federal agencies, similar to how a lockbox service processes payments for private businesses.

Why Other Options Are Incorrect:

* A. Zero-balance account:This refers to a type of bank account that maintains a balance of zero by automatically transferring funds as needed, unrelated to Pay.gov's purpose.

* B. Concentration system:Refers to pooling funds from multiple accounts into one central account, not payment processing.

* D. Data warehouse system:A data warehouse stores and organizes large amounts of data for analysis, unrelated to payment collection.

References and Documents:

* U.S. Treasury Pay.gov Website:Describes Pay.gov as an electronic lockbox for federal payment processing.

* GAO Financial Management Systems Guide:Highlights the role of electronic lockboxes like Pay.gov in improving efficiency.

質問 # 58

In an attestation engagement, which party would make an assertion about a subject matter?

- A. practitioner

- B. management

- C. auditor

- D. user

正解:B

解説:

What Is an Attestation Engagement?

An attestation engagement is a type of professional service where an independent practitioner (typically an auditor or CPA) evaluates and provides a report on assertions made by another party about a specific subject matter. These engagements follow standards set by organizations like the AICPA or GAO.

Who Makes the Assertion?

* Management's Role:Management is the party responsible for making an assertion about the subject matter under review. For example, management might assert that internal controls are effective or that financial statements are fairly presented.

* Auditor/Practitioner's Role:The auditor or practitioner examines the evidence related to the assertion and provides an opinion or conclusion based on that examination.

* User's Role:The users are the stakeholders (e.g., investors, regulators) who rely on the practitioner's report, but they do not make assertions.

Why Other Options Are Incorrect:

* B. Auditor/Practitioner:The auditor or practitioner evaluates the assertion made by management, not the other way around.

* C. Practitioner:See above-practitioners don't make assertions.

* D. User:Users are the intended audience of the attestation report, not the party making assertions.

References and Documents:

* AICPA Attestation Standards (SSAEs):Clarifies the role of management in making assertions during attestation engagements.

* GAO's Government Auditing Standards (Yellow Book):Provides additional guidance on the roles of parties in attestation engagements.

質問 # 59

Which of the following would auditors issue an opinion on?

- A. performance audits

- B. forensic audits

- C. compliance audits

- D. financial statement audits

正解:D

解説:

* Audit Opinions:

* Auditors issue opinions onfinancial statement auditsto provide assurance about whether the financial statements are presented fairly in accordance with applicable accounting standards (e.g., GAAP).

* Other types of audits, such as performance or forensic audits, do not typically result in opinions but may provide findings or recommendations.

* Explanation of Answer Choices:

* A. Performance audits: These assess efficiency, effectiveness, or economy but do not include an opinion.

* B. Compliance audits: These assess adherence to laws or regulations and may include findings but not an opinion.

* C. Financial statement audits: Correct. These audits include an auditor's opinion on the fairness of the financial statements.

* D. Forensic audits: These focus on fraud investigation and result in findings, not an opinion.

:

AICPA,Audit Opinions on Financial Statements.

GAO,Government Auditing Standards (Yellow Book).

質問 # 60

Earned value management is preferred over traditional project management because

- A. earned value management provides information about status of deliverables, funds and time expended.

- B. traditional project management provides information about status of deliverables, funds and time expended.

- C. traditional project management is used to monitor progress and deliverables of larger projects.

- D. earned value management is used to monitor progress and deliverables of smaller projects.

正解:A

解説:

What Is Earned Value Management (EVM)?

* EVMis a project management methodology that integrates scope, cost, and schedule to measure project performance. It provides a comprehensive view of progress by combining information about deliverables (work completed), funds (budget spent), and time (schedule adherence).

Why Is EVM Preferred Over Traditional Project Management?

* EVM offers a holistic view of project performance by quantifying progress and comparing it to planned performance, allowing for proactive decision-making.

* Traditional project management often focuses on individual aspects (e.g., timelines or budgets) without integrating them as effectively as EVM.

Why Other Options Are Incorrect:

* A. EVM monitors smaller projects:EVM is not restricted to small projects; it is widely used for complex, large-scale projects.

* C. Traditional project management is used for larger projects:This is incorrect-both methodologies can be used for projects of any size.

* D. Traditional project management provides status on deliverables, funds, and time:This is inaccurate; traditional methods often lack the integrated performance tracking provided by EVM.

References and Documents:

* GAO Guide to Project Management:Recommends EVM for comprehensive performance tracking.

* PMBOK (Project Management Body of Knowledge):Details the advantages of EVM over traditional project management.

質問 # 61

Performance measures that relate program inputs to program outcomes are called

- A. process measures.

- B. activity measures.

- C. efficiency measures.

- D. cost-effectiveness measures.

正解:D

解説:

* Definition of Cost-Effectiveness Measures:

* Cost-effectiveness measures assess therelationship between inputs (resources used)and outcomes (results achieved)to determine whether a program delivers value for the resources invested.

* Explanation of Answer Choices:

* A. Efficiency measures: Incorrect. These relate inputs to outputs, focusing on how efficiently resources are used to produce services, but not directly tied to outcomes.

* B. Process measures: Incorrect. These measure activities or steps within a program but do not assess outcomes.

* C. Cost-effectiveness measures: Correct. These directly link inputs to outcomes, measuring the program's effectiveness in achieving its objectives relative to costs.

* D. Activity measures: Incorrect. These track the level of activity or effort but not outcomes or effectiveness.

:

GASB,Performance Measurement and Reporting for Government Programs.

GAO,Best Practices in Measuring Program Effectiveness.

質問 # 62

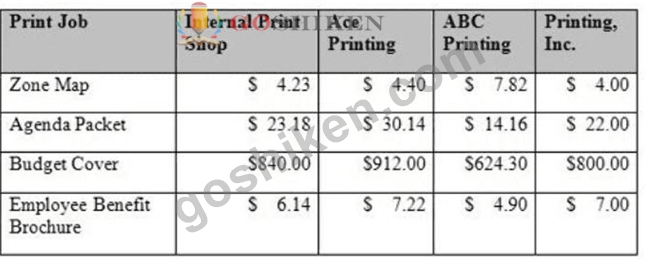

Based on the data below, what can be concluded about outsourcing print job?

- A. It is better to keep the printing in-house.

- B. Outsourcing printing is feasible.

- C. Outsourcing printing is necessary.

- D. ABC Printing should be awarded the outsourcing contract.

正解:B

解説:

* Understanding the Scenario:The table compares the costs of four printing jobs performed by an

"Internal Print Shop" versus three external vendors (Ace Printing, ABC Printing, and Printing, Inc.).

Each vendor's pricing varies by print job type. The task is to evaluate whether outsourcing (hiring external vendors) is a reasonable alternative to keeping the work in-house.

* Key Considerations in Outsourcing:According to governmental accounting principles and budgeting practices outlined by theAssociation of Government Accountants (AGA), the decision to outsource should consider:

* Cost-effectiveness: Does outsourcing reduce costs without compromising quality or service delivery?

* Operational efficiency: Can outsourcing free up internal resources for other priorities?

* Comparative pricing: How do external vendor rates compare to internal costs for identical services?

* Analysis of the Print Jobs:Let's break down the cost comparison for each print job:

* Zone Map:Internal cost = $4.23.Cheapest vendor = Printing, Inc., at $4.00.Outsourcing is cheaper for this job.

* Agenda Packet:Internal cost = $23.18.Cheapest vendor = Printing, Inc., at $22.00.Outsourcing is cheaper for this job.

* Budget Cover:Internal cost = $840.00.Cheapest vendor = ABC Printing, at $624.30.Outsourcing is significantly cheaper for this job.

* Employee Benefit Brochure:Internal cost = $6.14.Cheapest vendor = ABC Printing, at $4.90.

Outsourcing is cheaper for this job.

* Conclusion Based on Analysis:

* Across all four print jobs, the lowest-cost external vendor always beats the Internal Print Shop's costs.

* From abudgetary perspective, outsourcing is feasible as it offers cost savings across all jobs.

* Why Not A, C, or D?:

* Option A(Keep printing in-house): Incorrect, as in-house costs are consistently higher than the cheapest external vendor.

* Option C(Outsourcing is necessary): Incorrect, as feasibility doesn't mean necessity; internal printing is still an option if other factors (like quality or control) outweigh costs.

* Option D(Award contract to ABC Printing): Incorrect, since the best vendor depends on the job (e.g., Printing, Inc. is cheaper for Zone Map and Agenda Packet).

:

Association of Government Accountants (AGA),Government Financial Manager Certification Study Guide:

Budgeting, Cost Accounting, and Auditing Principles.

Government Finance Officers Association (GFOA),Best Practices in Outsourcing and Procurement.

Federal Accounting Standards Advisory Board (FASAB),Cost Accounting Standards for Governmental Operations.

質問 # 63

A city parks department is selecting a contractor to renovate a community playground. Which of the following contractors should be selected?

- A. The contractor with the second-lowest bid, who has no prior violations and meets all bid specifications.

- B. The contractor with the lowest bid who has a history of delayed projects.

- C. The contractor with the highest bid, who includes luxury, non-requested upgrades to the design.

- D. The contractor whose bid was submitted past the deadline but offers a discount for early payment.

正解:A

解説:

* Understanding the Procurement Process for Contractors:

* When selecting contractors for government projects, the goal is to ensure the selection of a responsible and responsive bidderwho meets all requirements outlined in the Request for Proposal (RFP) or bidding documents.

* Key considerations include the contractor's ability to meet deadlines, quality of work, and compliance with laws and regulations.

* Analyzing the Answer Options:

* A. The contractor with the lowest bid who has a history of delayed projects:While cost savings are important, a contractor with a history of delays poses a significant risk to project timelines and community satisfaction. This bidder is not considered "responsible" based on their track record.

* B. The contractor with the second-lowest bid, who has no prior violations and meets all bid specifications:Although this is not the lowest bid, it is the best choice because the contractor meets all requirements and has a clean history. Selecting a reliable bidder ensures the project is completed on time and within acceptable quality standards. This is the most responsible and justified decision.

* C. The contractor with the highest bid, who includes luxury, non-requested upgrades to the design:Selecting a contractor who proposes unnecessary and expensive upgrades is not cost- effective. Government procurement prioritizes fulfilling project specifications within the approved budget, making this choice impractical.

* D. The contractor whose bid was submitted past the deadline but offers a discount for early payment:Late bids violate procurement rules, which emphasize fairness and transparency.

Accepting this bid could lead to legal challenges or allegations of favoritism. Discounts do not justify breaching procurement guidelines.

* Why Option B is Correct:

* The second-lowest bid is the most responsible choice because the contractor:

* Meets all bid requirements.

* Has a strong history of compliance with regulations.

* Avoids risks associated with unreliable or excessively expensive options.

* This selection aligns with government procurement standards that prioritize balancing cost, quality, and reliability.

* References and Documentation from the Government Financial Manager (GFM) by AGA:

* Procurement Best Practices: The AGA emphasizes the importance of selecting bidders who demonstrate responsibility, reliability, and compliance with the bidding process.

* Ethical Procurement Standards: TheYellow Book (Government Auditing Standards) highlights the importance of fairness, transparency, and accountability in contractor selection.

* Source: AGA Certified Government Financial Manager (CGFM) study guides, Section IV:

Internal Controls, Procurement, and Ethics.

質問 # 64

As a way to ensure fiduciary responsiblity, a government entity should include which of the following in its investment policy?

- A. permissible and non-permissible investment securities

- B. historical allocations of investment securities

- C. key and non-key investment security controls

- D. prices and performance of its investment securities

正解:A

解説:

Why Include Permissible and Non-Permissible Investment Securities?

* Aninvestment policyoutlines the guidelines and restrictions for managing an entity's investments, ensuring compliance with laws and protecting public funds.

* Listingpermissible(e.g., government bonds, treasury securities) andnon-permissibleinvestments ensures clarity about what the entity can and cannot invest in, helping to mitigate risk and maintain fiduciary responsibility.

Why Other Options Are Incorrect:

* A. Prices and performance of investment securities:This information is important for monitoring investments but does not belong in the policy itself.

* C. Historical allocations of investment securities:Historical data informs decision-making but is not relevant to the rules governing investments.

* D. Key and non-key investment security controls:While controls are critical, they are part of the implementation process, not the investment policy.

References and Documents:

* GAO Investment Policy Guidelines:Recommends specifying permissible investments to ensure fiduciary responsibility.

* GFOA Best Practices in Investment Management:Emphasizes clear investment guidelines in the policy.

質問 # 65

The Parking Fund for a government entity has the following information in its Statement of Net Position.

Calculate the current ratio.

Total current assets$1,320

Total non-current assets$8,100

Total assets$9,420

Total current liabilities$ 810

Total non-current liabilities$ 360

Total liabilities$1,170

Total net position$8,250

- A. 1.14

- B. 0.98

- C. 1.63

- D. 0.61

正解:C

解説:

What Is the Current Ratio?

* Thecurrent ratiomeasures an entity's ability to cover its short-term liabilities with its short-term assets.

The formula is: Current Ratio=Total Current AssetsTotal Current Liabilities\text{Current Ratio} = \frac

{\text{Total Current Assets}}{\text{Total Current Liabilities}}

Current Ratio=Total Current LiabilitiesTotal Current Assets

Calculation:

* Total Current Assets = $1,320

* Total Current Liabilities = $810

Current Ratio=1,320810\text{Current Ratio} = \frac{1,320}{810}Current Ratio=8101,320 Current Ratio#1.

63\text{Current Ratio} # 1.63Current Ratio#1.63

Why the Current Ratio Matters:

* A current ratio above 1 indicates that the entity has more current assets than current liabilities, suggesting good short-term liquidity.

Why Other Options Are Incorrect:

* A. 0.61, B. 0.98, C. 1.14:These values result from incorrect calculations or misinterpretations of the formula.

References and Documents:

* GAO Financial Analysis Guide:Provides guidance on using the current ratio to assess liquidity.

* GASB Financial Reporting Requirements:Highlights the importance of liquidity measures in government financial statements.

質問 # 66

......

最新のGFMC試験問題集でAGA試験トレーニング:https://www.goshiken.com/AGA/GFMC-mondaishu.html

2026年最新のの問題GFMC問題集で最新のAGA試験を使おう:https://drive.google.com/open?id=194UP8S5sl0OrOdXTrT_7nFmSv5ph9IlM